While the COVID-19 pandemic briefly shaped housing policy with protections like mortgage forbearance, the challenges homeowners face today are driven less by temporary disruptions and more by persistent affordability issues. With inflation still elevated, home prices parked near record highs, and insurance costs climbing, more homeowners are running out of cushion—heightening the risk of mortgage delinquencies, as well as broader ripple effects on consumer spending and credit conditions. As budgets thin, questions about the sustainability of homeownership and the broader economic fallout are getting harder to ignore.

In a recent report, construction industry research firm Construction Coverage analyzed the latest data from the Consumer Financial Protection Bureau, Census Bureau, and Zillow to reveal the locations with the greatest percentage of mortgages at least 30 days delinquent.

It’s Tough Out There…

Homeowners across the U.S. are facing mounting financial pressures as inflation has driven up the costs of essential goods and services, including housing. With home prices remaining near all-time highs, it is increasingly difficult for many households to afford their mortgage payments and property taxes. Rising insurance costs add further strain to this situation, stretching budgets thin and raising concerns about the sustainability of homeownership.

As of Q2 2025, total mortgage debt in the U.S. stands at more than $12.9 trillion and accounts for more than 70% of the total debt held by U.S. households. Outstanding mortgage debt rose sharply during the pandemic—largely driven by below-average interest rates and elevated demand for housing—and it continues to rise to record levels in 2025.

Compared to mortgages, other consumer loan categories represent a much smaller proportion of total outstanding debt. Auto loans and student loans are the next largest loan types—each of which accounts for roughly 9% of total debt, or 18% combined. Credit card debt stands at approximately 6.6%, while HELOCs and other loan types comprise the remaining 2.2%.

Data from the New York Fed highlights how COVID-era financial assistance programs like loan forbearance, direct relief payments, and enhanced unemployment benefits worked to stave off loan delinquencies. Over the course of 2020 and 2021 when these programs were in effect, the percentage of loan balances at least 30 days delinquent dropped to historically low levels across all major loan types. Delinquent mortgage balances, for example, experienced a substantial drop from a pre-pandemic rate of 3.50% to a low of 1.39% in Q3 of 2021. Similar trends were observed for credit cards, auto loans, student loans, and HELOCs to varying degrees.

Unfortunately, a combination of elevated interest rates and the end of most federal and state-level enhanced benefits programs has led to increased frequencies of missed payments, especially for student loans. As of August 2024, the Department of Education has ceased enrollment in any of the various student loan repayment relief programs, and the U.S. Department of Treasury began notifying defaulted borrowers of their repayment options—which could lead to wage garnishment if loan balances are not repaid—on May 5, 2025.

Although student loan delinquencies saw the most dramatic shift, loan balance delinquency rates for all major loan types have surpassed pre-pandemic levels. Delinquent mortgages are also on the rise despite many homeowners buying or refinancing before 2022 and locking in low rates. As of Q2 2025, the share of mortgage balances over 30 days delinquent has risen to 3.68%.

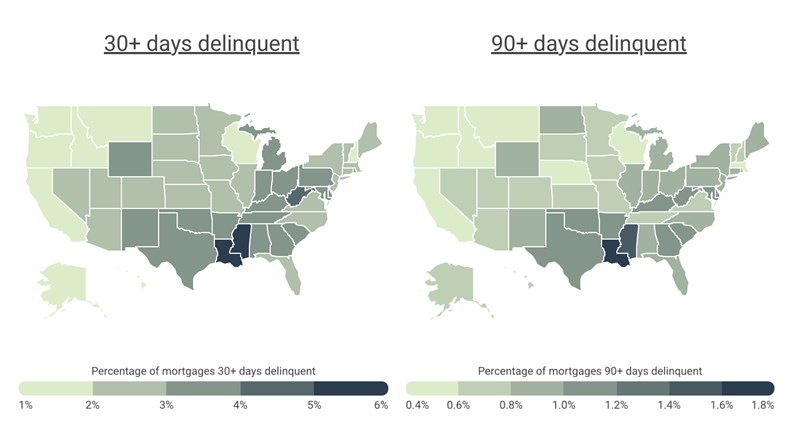

While mortgage delinquency rates are on the rise nationally, the concentration of delinquent mortgages varies significantly by location. In general, delinquency rates tend to be highest in areas with higher levels of unemployment and poverty, lower levels of income, and lower property values.

Regionally, states in the South and pockets of the East Coast tend to have the highest delinquency rates. For example, Louisiana, Mississippi, and West Virginia are the top three states for both 30-day and 90-day mortgage delinquencies. Other states with high rates of missed payments include Alabama and Texas. At the opposite end of the spectrum, the West Coast has the lowest share of mortgages more than 30 days delinquent, with Washington, Oregon, and California all reporting rates of delinquent mortgages under 2%.

Similar trends hold at the local level with major metropolitan areas in the South—like San Antonio, Memphis, Houston, and Birmingham—reporting high rates. Residents in West Coast metros like San Jose, San Francisco, and San Diego, on the other hand, are far less likely to miss a mortgage payment.

Key Findings for the New York Metro

- NY Metro Delinquency Rates: In the NY metro, 2.5% of mortgages were at least 30 days delinquent as of December 2024, which places the NY metro 29th worst among 53 large U.S. metros. Meanwhile, 0.8% were at least 90 days delinquent.

- Geographic Divide: Southern states like Mississippi and Louisiana report the highest rates of missed mortgage payments, while West Coast states like Oregon and California have the lowest. Similar patterns appear at the metro level, with higher delinquency rates in the South and pockets of the East Coast.

- Debt Is on the Rise Nationwide: Delinquency rates for all major loan types—including auto, student, and credit card debt—have now surpassed pre-pandemic levels. Mortgage loans dominate, however, accounting for over 70% of all U.S. household debt and totaling more than $12.9 trillion.

According to the data for New York-Newark-Jersey City, NY-NJ:

Percentage of mortgages 30+ days delinquent: 2.5%

Percentage of mortgages 90+ days delinquent: 0.8%

Unemployment rate: 5.1%

Median home value: $712,394

Median household income: $95,220

For reference, here are the statistics for the entire United States:

- Percentage of mortgages 30+ days delinquent: 2.8%

- Percentage of mortgages 90+ days delinquent: 0.8%

- Unemployment rate: 4.2%

- Median home value: $368,581

- Median household income: $77,719

The housing market plays a crucial role in the broader economy, influencing consumer spending and financial security. As homeowners now face rising costs and financial pressures, these challenges could have far-reaching implications for economic growth and stability.

{kind=link}

Leave a Comment