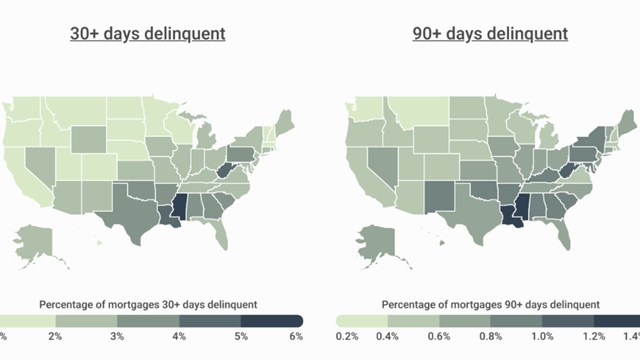

Given that we’re only just approaching the midpoint of the nation’s 15-day pause to stop the spread of coronavirus/COVID-19 (with extensions of stay-at-home orders and business closings looking likely), it may feel premature to talk about what we may expect when the crisis ends. But people most certainly are talking about the post-pandemic market -- with the topic becoming even more relevant on Monday, March 23, when President Trump seemed to suggest via Twitter that he’s considering relaxing the restrictions currently in place to slow the spread of the deadly disease.

How does that relate to the real estate market? The Cooperator spoke with a trio of industry experts to determine what direction urban housing markets in New York and across the nation may take as the crisis hopefully subsides. The first question is, how much of what may be ahead for the real estate market will be a direct result of the crisis, and how much may be attributable to underlying factors and forces that predated the pandemic?

What Was Happening Before Covid-19 Arrived?

While the arrival of the worst infectious pandemic in over a century has caused the abrupt shutdown of huge swaths of economic activity in New York City and many other urban markets, New York real estate was already experiencing a slowdown, mostly as a result of previous changes to tax laws at federal, state and local levels. The most severe effects were generally felt to be the result of changes in the treatment of state and local (SALT) taxes at the federal level, which has been acknowledged by many national experts as a serious depressant on home prices and values in all states negatively impacted -- particularly New York, New Jersey, California, and Illinois.

Jonathan Miller, President and CEO of Miller Samuel, a national real estate and appraisal firm based in New York, observes that in the two years since the enactment of the new tax law, the co-op and condo market has begun to adjust to its new reality. He believes that prices and market conditions were stabilizing before the new coronavirus exploded onto the world stage.

What the virus has triggered in our economy is not like the normal economic slowdowns, or even the recession that are to be expected over long enough periods of time; rather, it’s been an abrupt economic interruption. Such an interruption may in turn trigger a slowdown or a recession -- possibly even a depression -- but at the same time, as Miller explains, “If the crisis winds down by the end of the second quarter, we may well see a rebound in the third quarter as a result of pent-up demand.” The simple fact is that the underlying factors affecting the market may, and perhaps will, come back into play when the current crisis is over, at least in the short term.

Long-Term Structural Changes

David Eisenbach is a professor of history, media and politics at Columbia University in New York City. He is also active in local politics, and recently ran for New York City Public Advocate. Eisenbach takes a longer view of how the current crisis will affect the real estate industry. “The business and government leaders of New York have taken a long-term bet on speculative development for housing stock in New York City,” he says. “That will change as a result of the current crisis.”

Basically, he explains, the growth of residential markets in New York City has depended on creating residential product for super-wealthy individuals who invest their capital in high-end real estate: primarily luxury condo units, many of which are never even moved into. Production of more affordable units was sacrificed to attract these outsiders at the high end of the market. Going forward, Eisenbach argues that these wealthy individuals may be less likely to view New York City as a desirable place to park their investment funds if the city appears to be subject to negative events like contagion pandemics. He also agrees that the market was already weak due to the negative effects of the aforementioned tax law changes. He believes the present crisis may offer an opportunity for the city administration to restructure its approach to residential real estate development, and perhaps to reorient it toward programs that provide affordable housing for actual residents, rather than absentee investors.

Another View

Terence Tener is the CEO of KTR Real Estate Advisors, another New York-based national real estate appraisal and advisory firm. Tener sees Miller and Eisenbach’s positions, though diametrically opposed, as ultimately reconcilable. He agrees with Miller that should the current crisis resolve in a relatively short time -- say by the end of the second quarter -- co-ops and condominium units, the bedrock of the New York residential market, should experience a lift from pent-up demand from buyers whose house-hunting efforts were derailed by the stay-at-home orders now in effect. Alternatively, he does concur that the recent tax restrictions at all levels are a “death knell” for the New York market, particularly at the upper end, and points out that the expansion of the luxury ‘mansion tax,’ was already depressing sales. Tener goes on to point out that in the general market, legislation passed in June 2019 with respect to rents and rentals has also cast a pall over the residential sector of the property market beyond the co-op and condo sectors.

In short, according to the three experts consulted for this piece, we are at a crossroads. Factors at play before the current crisis had competing effects on the co-op and condo markets across all sectors. Those effects have been amplified by the current and acute coronavirus pandemic. What will happen in both the short and long term remains to be seen of course, but one thing seems for certain; uncertainty will be with us for quite some time -- and uncertainty is never market-friendly.

A J Sidransky is a staff writer/reporter for The Cooperator, and a published novelist.

{kind=link}

Leave a Comment