Every condo and co-op has its own set of governing documents by which building administrators direct their community's day-to-day business. Bylaws, rules and regulations, and precedent-setting legal cases help keep boards within the letter of the law, and offer a framework within which they can operate consistently from year to year.

Several laws apply to real estate in New York: for example, condos are governed by the New York Condominium Act, and the Real Property Actions and Proceedings Law (RPAPL) deals with landlord-tenant issues between a co-op and its shareholders. Case law interprets these statutes and sets legal precedent for co-op and condo owners; indeed the law governing co-ops in New York is mostly created by judge-made case law.

One statute originally created to regulate businesses, the Business Corporation Law—or BCL, for short—primarily governs how cooperative corporations, including housing co-ops, must be run.

The BCL provides specific rules regulating the corporate governance practices of co-ops, including the manner in which boards and shareholders conduct meetings, amend bylaws, and vote, and the BCL prescribes the rights and responsibilities of boards and shareholders. While it may be asking a lot of volunteers to pore over the entire BCL or know its nuances by heart, it's a good idea for all board members to at least be aware of its existence, and better to have a passing familiarity with its contents.

History and Background

The BCL was implemented over a century ago to regulate governance of corporations in New York, and remained more or less unchanged until it was overhauled in 1998. “The BCL was drafted generally for corporations, [the legislature] didn’t have co-ops in mind, and the courts have applied the BCL to co-ops,” explains Stephen M. Lasser, an attorney shareholder with the Manhattan office of the law firm Stark & Stark.

What happens if a co-op’s bylaws are inconsistent with the BCL? The BCL provides that when there is a conflict, the BCL will prevail: “The bylaws may contain any provision relating to the business of the corporation, the conduct of its affairs, its rights or powers or the rights or powers of its shareholders, directors or officers, not inconsistent with this chapter or any other statute of this state or the certificate of incorporation.” The BCL is a default set of rules.

“If the governing documents are silent on a particular matter then you have to look to the BCL,” says Lasser. “Oftentimes, the bylaws will track the language in the BCL, but you can’t assume that’s always the case. In some instances, there are provisions of the BCL that would trump.”

For example, if a lease has a requirement that contradicts the BCL, the BCL would trump the contradicting provision in the lease. “When you are making a corporate decision you have to look at the governing documents and see whether or not the documents were drafted in contradiction with the BCL,” according to Lasser.

Only one section of the BCL was drafted specifically for co-ops, a section pertaining to flip taxes. “Although the BCL was not drafted with co-ops in mind,” says Lasser, “Section 501 of the BCL was revised in 1986 to deal with a legal issue unique to co-ops, the imposition of flip taxes. Specifically, BCL 501(c) provides an exception to the rule that all shares be treated equally and allows co-ops to impose flip taxes that are not based on the number of shares owned by a selling shareholder.”

While the BCL was not created initially for co-ops, most co-ops are organized under the statute. “In my experience, 99 percent of the cooperative housing corporations are organized under the BCL,” says attorney Richard Siegler, a partner with Manhattan-based law firm Stroock & Stroock & Lavan LLP. “There’s only one co-op I have ever represented which was organized under the Cooperative Corporations law of New York State.” That particular co-op, according to Siegler, was established in the 1960s and had approximately 3,000 units. “Because of certain unique characteristics,” Siegler says, “it was organized under a law that was designed basically for agricultural cooperatives.”

Other states such as Florida and New Jersey have statutes designed specifically for cooperative housing corporations. However, New York’s BCL, drafted for business corporations in general, seems to adequately address the issues of co-op corporate governance. “If it ain’t broke you don’t fix it,” says Siegler. “For all these years, co-op housing corporations have been governed by the BCL even though it’s not specific to them, and as a result, I don’t think it’s necessary to enact a cooperative housing corporation law.”

Shareholder Rights &

Board Responsibilities

Which parts of the BCL are most important for co-op boards and shareholders to be informed about? According to Siegler, there are two sections of the BCL for boards and shareholders to pay close attention to: Article 6, which deals with shareholder rights, and Article 7, which deals with how the corporation is managed, explaining the rights and responsibilities of directors and officers.

“Under the BCL, any shareholder has standing to review certain important building documents—such as financial statements, shareholder lists, or the minutes from shareholder meetings,” says attorney Bruce Cholst, a partner with the law firm of Rosen Livingston & Cholst LLP in Manhattan. “Shareholders may also make extracts from said documents, provided the review be for ‘any purpose reasonably related to such person’s interest as a shareholder.’ Shareholders also have the right under case law to review the corporation’s other books and records, so long as the inspection is sought in good faith and for a purpose consistent with the shareholder’s right to monitor his investment in the corporation.”

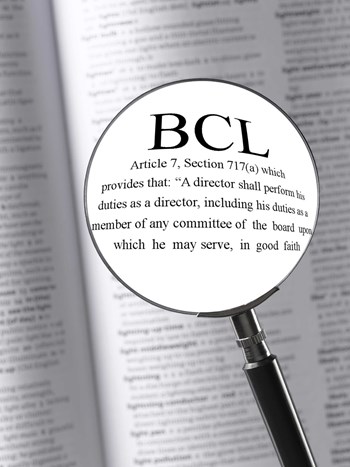

For example, if shareholders seek to challenge an action of the board, according to Siegler, they can invoke the BCL. Article 7, Section 717(a) of the BCL provides that “a director shall perform his duties as a director, including his duties as a member of any committee of the board upon which he may serve, in good faith and with that degree of care which an ordinarily prudent person in a like position would use under similar circumstances. In performing his duties, a director shall be entitled to rely on information, opinions, reports or statements including financial statements and other data…” Shareholders could potentially bring lawsuits under those provisions, Siegler says.

Shareholders and board members, however, should consult a lawyer before assuming that a board member has violated or satisfied his or her duty to act in “good faith.” Many terms in statutes become legal terms of art, which take on new meaning through judicial interpretation. The business judgment rule, which is not written into the BCL, is a doctrine of the courts, which largely shields the actions of board members.

Case Law

“Levandusky vs. One 5th Avenue Corp. (1990) is the seminal New York Court of Appeals case that held that the case law business judgment rule standard of judicial review, applicable to corporations generally, should apply to cooperative corporations,” says Lasser. The business judgment rule prevents judges from questioning actions of corporate directors "taken in good faith and in the exercise of honest judgment in the lawful and legitimate furtherance of corporate purposes." In other words, a court will not second-guess a director’s decision, even if it turned out to be a bad one, as long as the action was taken in good faith. Today, Lasser says, “all New York courts begin their evaluation of challenges of board decisions based on the analysis set forth in Levandusky to determine whether the business judgment rule should be applied.”

By acting in good faith directors can shield themselves from personal liability for actions taken in their capacity as a director. However, the indemnification provided by the BCL and the deference of the business judgment rule will not be available if there is an adjudication that establishes that the director acted in bad faith.

Board Meetings & Voting Requirements

In addition to outlining board responsibilities and shareholder rights, the BCL provides detailed regulations on the manner in which boards and shareholders conduct meetings and do business. The rules outlined in the BCL have the potential to empower shareholders to ensure their boards are performing lawfully. According to Siegler, shareholders can potentially bring lawsuits under Article 6 to assert their rights. “Suppose a co-op corporation doesn’t have an annual meeting for two years? Can a shareholder seek to have an annual meeting to elect new directors? The answer is yes—it’s in Article 6—they can have a special meeting to elect directors.”

As far as voting requirements, Article 6 of the BCL also provides that a majority of all outstanding shares is required to amend a co-op’s bylaws. A bill that passed the state Legislature shortly after the 1998 overhaul further reduced the requisite vote for amending co-op bylaws to a bare majority of the votes cast at a shareholder’s meeting at which a quorum is present,” says Cholst. “In addition, a resolution by the board (without shareholder approval) to the extent authorized in the co-op’s bylaws or its Certificate of Incorporation may also amend bylaws. However, any such board-enacted bylaw is subject to repeal by vote of the shareholders.”

The BCL also permits shareholder action by less than unanimous (but not less than majority) written consent if the certificate of incorporation so provides. All written consents must be signed within 60 days. Notice of any action taken in this fashion must be provided to those shareholders that did not issue their written consent. “Boards may wish to take advantage of this aspect of the law, which obviously facilitates the shareholder approval process, by enacting the appropriate amendment to their Certificate of Incorporation; such an amendment requires approval by both the board an the shareholders,” says Cholst.

For shareholder meetings, Section 602 of the BCL allows cooperatives to create their own rules in the bylaws, as these meetings “may be held at such place, within or without this state, as may be fixed by or under the bylaws, or if not so fixed, at the office of the corporation in this state.” The BCL does prescribe, however, that annual meetings must be held for the election of directors and transaction of other business. Meetings via conference call or video conference are now permitted by the BCL as long as everyone in the meeting can hear each other at the same time.

“The BCL does not deal explicitly with issues such as who presides during meetings, what parliamentary rules govern, nominating procedures, proper format for committee reports, the method and timing of notices, the format of proxies, or methods by which questions from the floor are fielded,” according to Cholst. “The absence of clear-cut guidelines regulating the precise manner in which shareholder meetings are noticed and conducted often lead to confusion and sometimes rancor at shareholder meetings. This is particularly the case when insurgent shareholders perceive that the rules are being arbitrarily applied for the sole benefit of the incumbent board.”

Other important provisions of the BCL pertain to the election process, the form of proxies, and the treatment of abstentions.

The Future of the BCL

As of this writing, we can expect to hear about New York’s BCL more than we usually do. According to property manager Michael Berenson, president of Manhattan-based management firm AKAM Associates, Inc., a recent proposal coming from the federal government would place restrictions on the imposition of private transfer fees, commonly called flip taxes.

“The recently-proposed Federal Housing Finance Agency (FHFA) ruling would prohibit Fannie Mae or Freddie Mac from purchasing loans in co-ops where there is a transfer fee/flip tax or other similar revenue-generating device,” Berenson notes.

Opponents from all over the co-op world are lining up to challenge this proposal. “First there is the argument that transfer fees/flip taxes have historically been a boon to co-ops,” says Berenson. “Second is the fact that Section 501(c) of New York’s Business Corporation Law permits transfer fees/flip taxes. To do away with transfer fees/flip taxes would not only hurt the residential cooperative corporations that rely on them for important income, but also would affect a right derived from the Business Corporation Law, which no doubt will be invoked as the debate about FHFA’s restrictive proposal becomes more public.”

Because all shareholders in a cooperative have rights and duties under the BCL, it is wise for board members and shareholders alike to familiarize themselves with this body of law, instead of only relying on the bylaws of the cooperative. The text of the law is available on the New York Legislature website at http://public.leginfo.state.ny.us/menuf.cgi under “Laws of New York.” Board members and shareholders should look most closely at Article 6, titled “Shareholders,” and Article 7, titled “Directors and Officers.” Shareholders and board members should beware, though, that the law is extensive, and to properly understand the law and to deal with potential issues, a lawyer should be consulted.

Elizabeth Ilene Robbins is a freelance writer and a June 2010 graduate of the Benjamin N. Cardozo School of Law.

{kind=link}

37 Comments

Leave a Comment